What is GST Appeal?

The requirement of appeal under GST comes from disagreement in demand order passed by the adjudicating authority of the department.

The first level of appeal against the order of adjudicating authority can be filed by aggrieved person, under Section 107 of the CGST Act, 2017 which is referred to as appeals to appellate authority. This authority is also referred to as First Appellate Authority. Aggrieved person may or may not be registered under GST Act.

This first level of appeal can also be filed by the Commissioner against the order of adjudicating authority if he is of the opinion that the order that has been passed by the adjudicating authority are legally incorrect or prejudicial to the interest of the revenue or has not taken into account certain material facts. This appeal filed by the department is also called the Review Application.

Time limit for filing GST Appeal?

Time limit for filing GST Appeal by aggrieved person is 3 months from the date of communication of such decision/order. However, 1 month condonation can be granted to such person on showing relevant grounds of delay to the appellate authority.

Time limit for filing GST Appeal by the Commissioner is 6 months from the date of communication of the decision/order. However, 1 month condonation can be granted to department on showing relevant grounds of delay to the appellate authority.

Form and Procedure for filing GST Appeal?

Form of GST Appeal for Aggrieved person

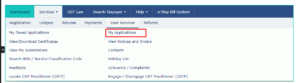

An appeal to Appellate Authority by the aggrieved person shall be filed in FORM GST APL-01. FORM GST APL-01 is to be filed electronically as per sub-rule (1) of rule 108 of the CGST Rules, 2017. After logging into GST portal, go to services, then user services and then my applications. On “My applications” page, select application type as ‘Appeal to Appellate Authority’ and then click on ‘New Application’.

A certified copy of the decision or order appealed against shall be submitted within 7 days of filing the appeal under sub-rule (1) of rule 108 of the CGST Rules, 2017 and a final acknowledgement, indicating appeal number shall be issued thereafter in FORM APL-02 by the Appellate Authority.

Form of GST Appeal for Department

An appeal to Appellate Authority by the Commissioner or officer authorized by him shall be filed in FORM GST APL-03. FORM GST APL-03 is to be filed electronically as per sub-rule (1) of rule 109 of the CGST Rules, 2017.

A certified copy of the decision or order appealed against shall be submitted within 7 days of filing the appeal under sub-rule (1) of rule 109 of the CGST Rules, 2017 and a final acknowledgement, indicating appeal number shall be issued thereafter in FORM APL-02 by the Appellate Authority.

Format of APL-01?

Format of APL-01 is available in CGST Rules, 2017 (Part-B Forms). Click here to access it.

What is the difference between Statement of facts for GST Appeal and Grounds of appeal in GST?

Statement of facts covers all the facts of the case as is agreed by both the aggrieved person and the adjudicating authority and also contain the details regarding the points that are in dispute whereas the grounds of appeal contain the details regarding the reason filing appeal for the points that are in dispute.

How to write Statement of facts in GST Appeal?

Statement of fact covers all the facts of the case. The statement of facts should start with a brief about the nature of business activities undertaken by the aggrieved person.

The statement of fact should clearly bring out the points of the case which are in dispute. The points which may be in dispute may be of the one or more of the following –

-

Misclassification of any goods or services or both

-

Wrong applicability of a notification issued under the provisions of the Act

-

Incorrect determination of time and value of supply of goods or services or both

-

Incorrect admissibility of input tax credit of tax paid or deemed to have been paid

-

Incorrect determination of the liability to pay tax on any goods or services or both

-

Whether the applicant is required to be registered

-

Whether any particular thing done by the applicant results in supply of goods or services or both

-

Rejection of application for registration on incorrect ground

-

Cancellation of registration for incorrect reasons

-

Transfer/Initiation of recovery/Special mode of recovery

-

Tax wrongfully collected/Tax collected not paid to Government

-

Determination of tax not paid or short paid

-

Refund on wrong ground/Refund not granted/Interest on delayed refund

-

Fraud or willful suppression of fact

-

Anti-profiteering related matter

-

Others

The tone word used should be truthful and neutral, i.e. the tone should not be positive or negative.

How to write grounds of appeal in GST to win the decision in your favour?

The tone of the appeal should be respectful.

Starting words of the paragraph can be “It is most respectfully submitted that” and should be followed by the details of the case stating the exact point/s of dispute.

There should be use of legal maxims and relevant case laws to support the case.

In case of writing grounds of appeal in GST, the most commonly used legal maxim is “LEX NON COGIT AD IMPOSSIBILIA”, means the law does not compel a man to do what he cannot possibly perform. In GST Laws, a lot of responsibility is cast upon the recipient of goods or services or both before he can take the input tax credit (ITC) of such goods or services or both. The GST law on various occasions is going against this legal maxim i.e. LEX NON COGIT AD IMPOSSIBILIA. Instances where this legal maxim can be used are –

-

Denial of ITC due to mismatch between GSTR-3B and GSTR-2B before 1-1-2022. Since 1-1-2022 complete matching of GSTR-2B and GSTR-3B has been made a part of CGST Act, 2017 and corresponding rules.

-

Denial of ITC due to non-payment of ITC by the supplier of goods or services or both as per section 16(2) of the CGST Act, 2017.

Use of legal maxims and case laws gives strong support to the case and leads the conclusion in the favour of the aggrieved person.

Often it is seen that the demand order does not clearly speak out the grounds for rejecting the reply to the notice. Reply to Notice must have been filed by the aggrieved person during the course of proceedings under Section 73 or Section 74 of the CGST Act, 2017. The aggrieved person should re-emphasize on such points on which grounds for rejecting the reply have not been specified properly or have been totally ignored by the adjudicating authority.

Further a request can be made for quashing of demand order which was issued without issuing a speaking order. As per section 75(6) of the CGST Act, 2017, the proper officer, in his order, shall set out the relevant facts and the basis of his decision. In other words, there is requirement of the law to issue a speaking order with the details containing basis of his decision.

One can further assists his/her case by bringing out bona-fide intentions of the aggrieved persons and portraying him/her as law abiding citizen of India.

How to write prayer in GST Appeal?

The aggrieved person should clearly set-out the prayer for GST Appeal. If the demand is unjust, then the prayer should be to quash the order of demand. If the demand is justified, then the prayer could be to set-aside the penalty being a bona-fide case.

Pre-deposit in GST Appeal?

Pre-deposit for filing GST Appeal by Aggrieved person

There is a mandatory requirement under Sec 107 of the CGST Act, 2017 to furnish pre-deposit by an aggrieved person before he/she can upload the GST APL-01 form online. Amount of Pre-deposit is sum of

-

Admitted part – Full amount

-

Disputed part –

-

In case of CGST/SGST, 10% of remaining amount of TAX (not interest/penalty) in dispute (Maximum ₹ 25 crore)

BUT 25% of remaining amount of PENALTY in case of order u/s 129(3)

-

In case of IGST, 20% of remaining amount of TAX (not interest/penalty) in dispute (Maximum ₹ 50 crore)

-

On refund of Pre-deposit, interest u/s 56 shall be paid from the date of payment of the amount (and not from the date of order of the AA) till the date of refund.

Pre-deposit for filing GST Appeal by Department

There is no mandatory requirement under Sec 108 of the CGST Act, 2017 to furnish pre-deposit by the department before it can upload the GST APL-03 form online.

Frequently Asked Questions (FAQs)

Can an aggrieved person withdraw Appeal filed in GST? How do I cancel my GST Appeal?

Yes, an Appeal application can be withdrawn. To withdraw an Appeal application, click on to the Withdraw Appeal tab in the Case details page and select Withdraw Application from the Actions drop-down. A form will be displayed. Fill the form and click the Withdraw Appeal button. An appeal application can be withdrawn until a notice is issued or appeal order is passed. Once a notice has been issued, the application cannot be withdrawn.

Can I file Appeal application after it has been rejected at admission stage?

Yes, an appeal application can be re-filed after it has been rejected at the admission stage. To file the application, navigate to the New application page. Select the Order type and enter the Order ID of the original application. Fill in the form and Submit the application.

How many times can I re-file an Appeal application?

After an Appeal application has been rejected, it can be filed once more by the taxpayer.

Fees in GST Appeal?

There is no fee for filing GST Appeal at the first appellate authority.

![]()